Cash Back vs Points vs Miles: Which Credit Card Rewards Are Better in May 2026?

Compare cash back, points, and miles with a cash-equivalent formula, redemption examples, and when 3X points beats 3% cash back — plus cash back vs travel card choice.

Madeen compares public issuer terms with its card-rule catalog. Issuer pages control rewards, fees, benefits, exclusions, and eligibility; Madeen does not issue cards, make approval decisions, or provide financial advice.

Which cards show the cash back, points, and miles tradeoff?

- Rewards

- Earn 2% cash back on purchases: 1% when you buy and 1% as you pay, under current issuer terms.

- Annual fee

- $0

Pros

- Creates a clear cash benchmark for everyday purchases.

- No annual fee keeps the comparison simple.

- No category guessing for base purchases.

Cons

- Does not create outsized travel redemption upside.

- Other cards can beat it in specific bonus categories.

- Cash back is earned as ThankYou Points, so redemption method still matters.

Issuer terms are authoritative. Card links may point to issuer pages or approved partners when available.

Chase Sapphire Preferred Credit Card

Best example of flexible points with category bonuses and travel options

- Rewards

- Earn 3X points on dining and select streaming services, 2X on travel, and 1X on other purchases, with issuer-defined redemption options.

- Annual fee

- $95

Pros

- Flexible points can be redeemed in several ways.

- Dining and travel categories can beat flat cash back when valued conservatively.

- Points may be more useful for travelers than a fixed cash rebate.

Cons

- Annual fee means the extra value has to be real.

- Point value depends on redemption method.

- A flat cash-back card may be better for non-bonus purchases.

Issuer terms are authoritative. Card links may point to issuer pages or approved partners when available.

Capital One Venture Rewards

Best example of simple miles that still require a redemption assumption

- Rewards

- Earn unlimited 2X miles on every purchase, plus higher rates on eligible Capital One Travel bookings under current issuer terms.

- Annual fee

- $95

Pros

- Flat 2X earning is easy to remember.

- Miles can fit travelers who want statement-credit or transfer options.

- No category tracking for everyday spend.

Cons

- Miles are not the same as cash unless the redemption fits your plans.

- Annual fee raises the break-even point.

- Non-travel redemptions can be less attractive than travel-focused use.

Issuer terms are authoritative. Card links may point to issuer pages or approved partners when available.

Cash back, points, and miles can all be good rewards. The mistake is comparing only the headline number, such as 3%, 3X, or 2 miles per dollar. Those numbers use different units, so the better question is: what is each purchase worth after you convert the reward into a realistic cash-equivalent value?

The short version: compare credit card Cash Back, points, and miles by turning each reward into an estimated return. Cash back is usually easiest because 3% is already 3 cents per dollar. Points and miles need one more assumption: how much one point or mile is worth through the redemption option you will actually use after fees, caps, and restrictions. Browse per-card effective rates in the Madeen card directory or start with the Citi Double Cash card page as a cash-back benchmark.

How do you compare Cash Back, points, and miles?

Compare them with a simple formula:

Earn rate x estimated value per point or mile = estimated returnFor Cash back, the estimate is usually direct. A 2% cash-back card is worth about 2 cents per dollar before fees, caps, and exclusions. For points and miles, the same multiplier can mean different things. A 3X card is roughly a 3% return if each point is worth one cent to you. It is worth less if you redeem below one cent and more if you consistently redeem above one cent.

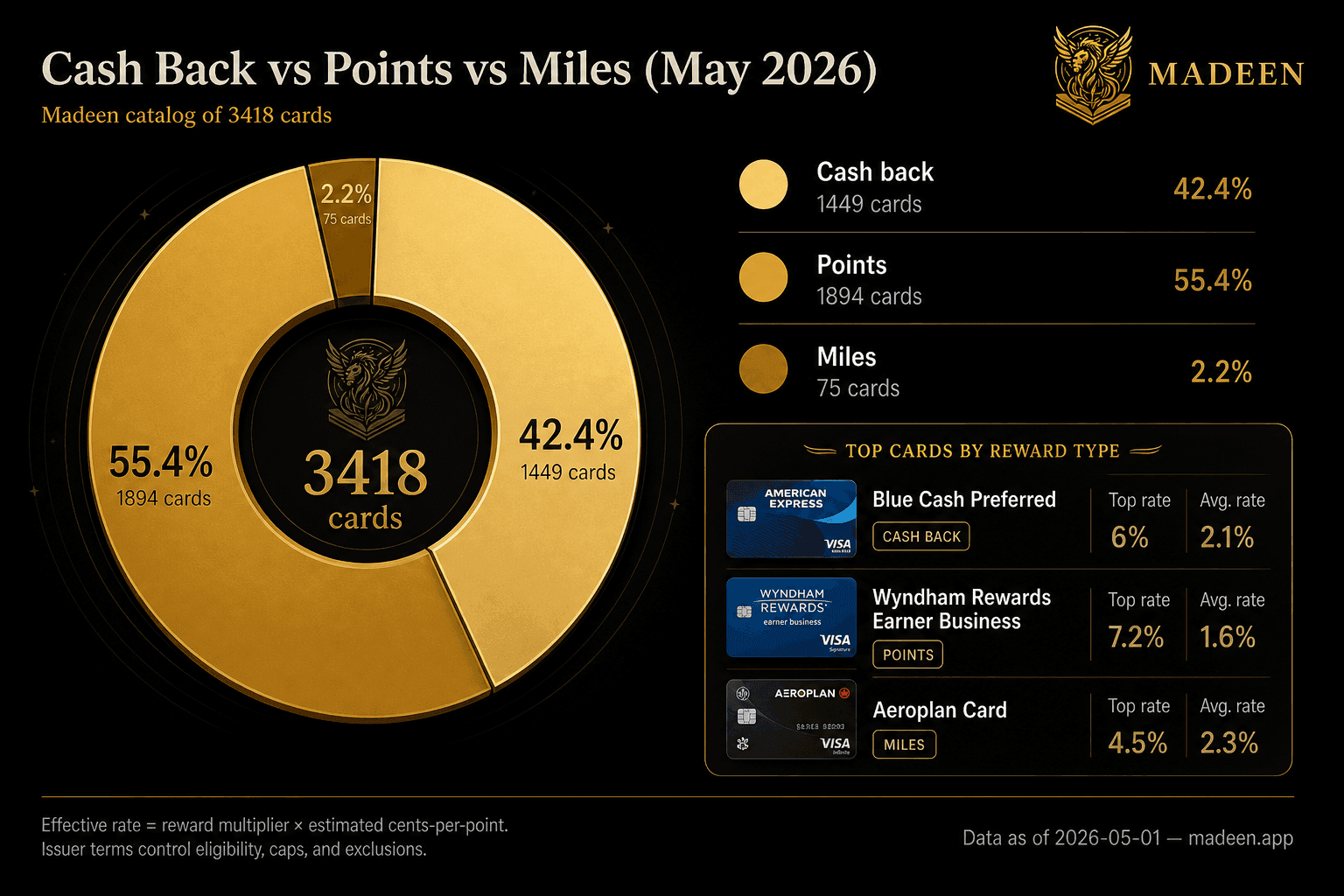

The Madeen Card Rules Index shows why this matters. Among 3,944 cards in the current catalog snapshot, 1,077 use Cash Back as the primary reward currency, 2,759 use points, and 108 use miles. Every card in that catalog has an estimated cash value per unit so Madeen can compare unlike currencies in one wallet-specific recommendation, but the estimate is still a practical assumption rather than an issuer guarantee. The methodology page explains how Madeen separates those estimates from issuer-controlled terms. For step-by-step CPP math, see how to value credit card points; for redemption paths after you earn points, see how to redeem credit card points; for a head-to-head points-card choice, compare Amex Gold vs Chase Sapphire Preferred.

Is 3X points better than 3% Cash back?

3X points is better than 3% Cash back only when one point is worth more than one cent after you account for redemption method, fees, and category rules.

Here is the quick comparison:

| Reward | Assumed value | Estimated return |

|---|---|---|

| 3% Cash Back | 1 cent per cent of Cash back | 3.0% |

| 3X points | 0.8 cents per point | 2.4% |

| 3X points | 1.0 cent per point | 3.0% |

| 3X points | 1.25 cents per point | 3.75% |

That table is why “points are worth more” and “Cash back is always safer” are both incomplete answers. Points can beat Cash Back when the redemption is strong and realistic. Cash back can win when the points redemption is weak, inconvenient, capped, or tied to an annual fee that the rewards do not overcome.

Which cards show the difference in real life?

Use real cards as examples, not universal answers. The right card depends on what you already carry, where you spend, and how you redeem.

Citi Double Cash is a useful cash-back benchmark because its core pitch is simple: earn 1% when you buy and 1% as you pay, with no annual fee under current issuer terms. Citi also describes the rewards as ThankYou Points that can be redeemed for Cash back in forms such as statement credit, direct deposit, or check. That makes the card a clean baseline: if a points or miles card cannot beat this kind of simple return for your use case, the extra complexity may not be worth it.

Chase Sapphire Preferred shows why points can be better for the right traveler. Chase lists category bonuses such as 3X points on dining and 2X on travel, and Ultimate Rewards points can be used through Chase redemption options. If your realistic point value is one cent, 3X dining is about a 3% estimated return before the annual fee. If your redemption is worth more, it can beat a 3% cash-back card. If you redeem poorly or do not use the travel ecosystem, the value falls.

Capital One Venture Rewards shows the miles tradeoff. The card earns unlimited 2X miles on every purchase under current issuer terms, and Capital One describes travel-focused redemption options such as covering eligible travel purchases and using transfer partners. That can be attractive if you travel and redeem miles intentionally. If you want cash-like simplicity or rarely use travel redemptions, a miles card may be less straightforward than a flat cash-back card.

For flat-rate cash-back head-to-heads, compare Capital One Quicksilver vs Citi Double Cash, Citi Double Cash vs Wells Fargo Active Cash, and Chase Freedom Unlimited vs Discover it. Inside Chase, see Freedom Flex vs Freedom Unlimited and Citi Custom Cash vs Freedom Flex for category-card tradeoffs. For how quarterly 5% calendars and activation caps work, read how credit card rotating categories work.

How should you value credit card points?

Value points based on your likely redemption, not the best redemption someone else can find.

Use this conservative order:

- Cash or statement-credit value: Easy to understand, but sometimes lower than travel value.

- Travel portal value: Useful when you would book that travel anyway and the portal price is competitive.

- Transfer-partner value: Potentially higher, but only if you know how to use airline or hotel partners.

- Gift cards, merchandise, and checkout redemptions: Convenient, but values can vary and may be weaker.

- Aspirational examples: Good for learning, but risky as a default assumption.

If you are not sure, start with one cent per point for flexible points only when the issuer’s redemption options support that assumption for your use. For airline and hotel miles, be even more careful. Their value can depend on award availability, route, hotel category, taxes, fees, expiration rules, and whether you would have paid cash for the same trip.

How do redemption options change Cash Back value?

Cash back is easiest to compare when the redemption option acts like cash. Statement credits, bank deposits, and checks are usually the cleanest comparison points because they can be translated into cents per dollar with little extra judgment. Gift cards, shopping checkout redemptions, merchandise, and travel portals can be useful, but they may change the real value or lock you into a channel you would not otherwise use.

That matters for cards that advertise Cash back but issue rewards as points. Citi Double Cash is a good example: the card is marketed around cash-back earning, but Citi describes the rewards as ThankYou Points that can be redeemed in several ways. If you redeem those points for a strong cash-equivalent option, the comparison stays simple. If you choose a weaker redemption, the return is lower than the headline rate suggests.

The CFPB has also warned that rewards programs can create problems when redemption terms are unclear, benefits change after consumers make decisions, or advertised rewards are hard to actually use. That is why a cash-equivalent comparison should include both the earn side and the redemption side. A high multiplier is not enough if the practical redemption path is weaker than cash.

How do annual fees change the comparison?

Annual fees lower the effective return unless the card’s extra rewards and benefits exceed the fee. A $95 card can still be worth it, but the points or miles need to do more work than a no-fee cash-back card.

For example, a no-fee 2% cash-back card and a $95 2X miles card may look similar on headline earn rate. The miles card wins only if your redemptions, benefits, and travel fit create enough extra value to cover the fee. If you redeem the miles weakly or do not use the benefits, the no-fee cash-back benchmark may be better.

For a deeper fee framework, read Is a Credit Card Annual Fee Worth It?. The important point here is that reward currency and annual fee should be evaluated together, not separately.

Why does Madeen use estimated cash value?

Madeen uses estimated cash value so the app can compare cards in one practical ranking at checkout. A grocery purchase should not require you to manually compare 3% Cash Back, 3X bank points, 2X airline miles, and a base 2% card in your head.

The estimate lets Madeen translate each eligible reward rule into a common unit. That is especially useful because the catalog includes all three major reward currencies. In the current catalog, points are the most common primary currency, Cash back is close behind, and miles are less common but still important for travel cards. A common estimate keeps the recommendation readable while still reminding you that issuer terms and your redemption habits are authoritative.

Madeen does this locally. You select the cards you carry, and the app compares reward rules without asking for your bank login, card numbers, or transaction history. For the product mechanics, read how a credit card optimizer can work without bank login; for the broader launch context, read why Madeen does not ask for your bank login.

What is the safest way to choose between Cash back, points, and miles?

Choose the reward currency that you will redeem well with the least unnecessary complexity.

Use this checklist:

- Start with your best no-fee cash-back card as the baseline.

- Convert points and miles into a realistic estimated return.

- Subtract annual fees unless benefits clearly offset them.

- Check category caps, activation rules, and merchant exclusions.

- Prefer points or miles only when you understand the redemption path.

- Revisit the decision when issuer terms or your travel habits change.

Issuer terms are authoritative, and card rewards can change. Before applying for or relying on a card, review the issuer’s current rewards, fees, redemption rules, caps, exclusions, and benefit terms.

For category decisions where caps change the math, pair this framework with how credit card reward caps and limits work. For how cash-back earn and redemption work before you compare currencies, read how credit card cash back works. For a step-by-step CPP formula when comparing points cards to Cash Back, see how to value credit card points. For the card-type fork before currency math, read cash back card vs travel card. Rewards only keep full value when you pay statement balances — read what a credit card grace period is and why minimum payments erode returns. If merchant coding changes which category bonus applies, read how merchant category codes affect credit card rewards. For entertainment purchases where caps and coding collide, see the best credit card for sports tickets hub. For dining-heavy wallets choosing Cash back vs Membership Rewards, compare Capital One Savor vs Amex Gold. If you are still choosing your first rewards card, compare secured vs unsecured credit cards and Chase Freedom Flex vs Discover it before you optimize redemption math.

Related encyclopedia topics

Frequently asked questions

How do you compare cash back, points, and miles?

Convert each reward to an estimated cash value by multiplying the earn rate by a realistic value per point or mile. Then compare the result with a cash-back card you would actually use.

Is 3X points better than 3% cash back?

3X points is better than 3% cash back only if each point is worth more than one cent to you after fees, caps, and redemption limits. If each point is worth one cent, 3X and 3% are roughly equal before other costs.

How should you value credit card points?

Use the redemption you will realistically choose, not the highest advertised possibility. Cash, statement-credit, travel-portal, and transfer-partner redemptions can all produce different values.

Why does Madeen use estimated cash value?

Madeen uses estimated cash value so cash back, points, and miles can be compared in one checkout-time ranking. The estimate is a practical comparison tool, not a promise of what every redemption will be worth.

Should you always choose points or miles for travel?

No. Points and miles can be valuable for travel, but cash back may be better if you want simplicity, avoid annual fees, or do not redeem through the travel channels that make the points valuable.

Which cash back redemption option is easiest to compare?

Statement credits, bank deposits, and checks are usually easiest to compare because they behave most like cash. Gift cards, checkout redemptions, travel portals, and transfer partners need a separate value assumption.

Is it better to have cash back or miles?

Cash back is usually better when you want simple, flexible rewards and do not travel often enough to redeem miles well. Miles can beat cash back when you fly regularly and redeem at strong value, but weak mile redemptions often underperform a flat 2% cash-back card.

Is 5% cash back the same as 5X points?

No. Five percent cash back is five cents per dollar before caps and exclusions. Five points per dollar is only equivalent if each point is worth one cent to you through the redemption you will actually use—and many redemptions are worth less.

Sources and notes

- Madeen analysis Madeen card catalog reward-currency analysis - Madeen Accessed 2026-05-01.

- Issuer terms Citi Double Cash Credit Card - Citi Accessed 2026-05-01.

- Issuer terms How to Redeem Citi Double Cash Credit Card Rewards - Citi Accessed 2026-05-01.

- Issuer terms Chase Sapphire Preferred Credit Card - Chase Accessed 2026-05-01.

- Issuer terms Chase Ultimate Rewards: How Our Program Works - Chase Accessed 2026-05-01.

- Issuer terms Capital One Venture Rewards Credit Card - Capital One Accessed 2026-05-01.

- Issuer terms How to Earn and Redeem Capital One Miles - Capital One Accessed 2026-05-01.

- Regulator Consumer Financial Protection Circular 2024-07: Design, marketing, and administration of credit card rewards programs - Consumer Financial Protection Bureau Accessed 2026-05-21.