Is a Credit Card Annual Fee Worth It in May 2026?

Learn the simple break-even math for credit card annual fees, when a no-fee card is better, and how to value rewards, credits, and perks conservatively.

Madeen compares public issuer terms with its card-rule catalog. Issuer pages control rewards, fees, benefits, exclusions, and eligibility; Madeen does not issue cards, make approval decisions, or provide financial advice.

Which cards show common annual-fee tradeoffs?

Capital One Savor Cash Rewards Credit Card

Best example of a strong no-annual-fee everyday card

- Rewards

- Unlimited 3% cash back on dining, grocery stores, entertainment, and popular streaming services, with issuer exclusions.

- Annual fee

- $0

Pros

- No annual fee creates an easy break-even point.

- Simple cash back is easy to compare against fee cards.

- Covers several everyday categories.

Cons

- Lower ceiling than some premium points or capped category cards.

- Grocery rewards exclude superstores like Walmart and Target.

- Travel perks are limited compared with premium fee cards.

Issuer terms are authoritative. Card links may point to issuer pages or approved partners when available.

Blue Cash Preferred Card from American Express

Best example of a mid-fee card with a high everyday category rate

- Rewards

- 6% cash back at U.S. supermarkets on up to $6,000 per year in purchases, then 1%.

- Annual fee

- $95

Pros

- High supermarket cash back can overcome the fee for frequent eligible grocery spending.

- Cash back keeps the comparison straightforward.

- Useful if its other everyday categories also fit your wallet.

Cons

- Annual fee requires enough qualifying spend.

- U.S. supermarket rewards are capped each year.

- Issuer supermarket rules exclude some store types.

Issuer terms are authoritative. Card links may point to issuer pages or approved partners when available.

Capital One Venture X Rewards Credit Card

Best example of a premium travel card whose fee depends on using credits

- Rewards

- 2X miles on every purchase, higher rates through Capital One Travel, plus annual travel-credit and anniversary-mile benefits under current terms.

- Annual fee

- $395

Pros

- Premium benefits can offset much of the fee when actually used.

- Simple 2X base earning is broad.

- Useful for travelers who already book through Capital One Travel.

Cons

- High fee is hard to justify if travel credits or lounge benefits go unused.

- Travel-credit value depends on booking behavior.

- Miles value depends on redemption choices.

Issuer terms are authoritative. Card links may point to issuer pages or approved partners when available.

Annual fees are not automatically bad. They are also not automatically justified by a big rewards number, a welcome offer, or a list of perks. The right question is simpler: will this card beat the best no-fee card you would actually use?

The short version: a credit card Annual fee is worth it only when the extra rewards, statement credits, and benefits you will reliably use exceed the fee. If the math depends on optimistic travel redemptions, unused credits, or spending you would not otherwise make, a no-annual-fee card is usually the safer default.

Is a credit card Annual fee worth it?

A credit card Annual fee is worth it when the card produces more net value than a comparable no-annual-fee card. “Net value” means extra rewards plus usable credits and benefits, minus the Annual fee and any added complexity.

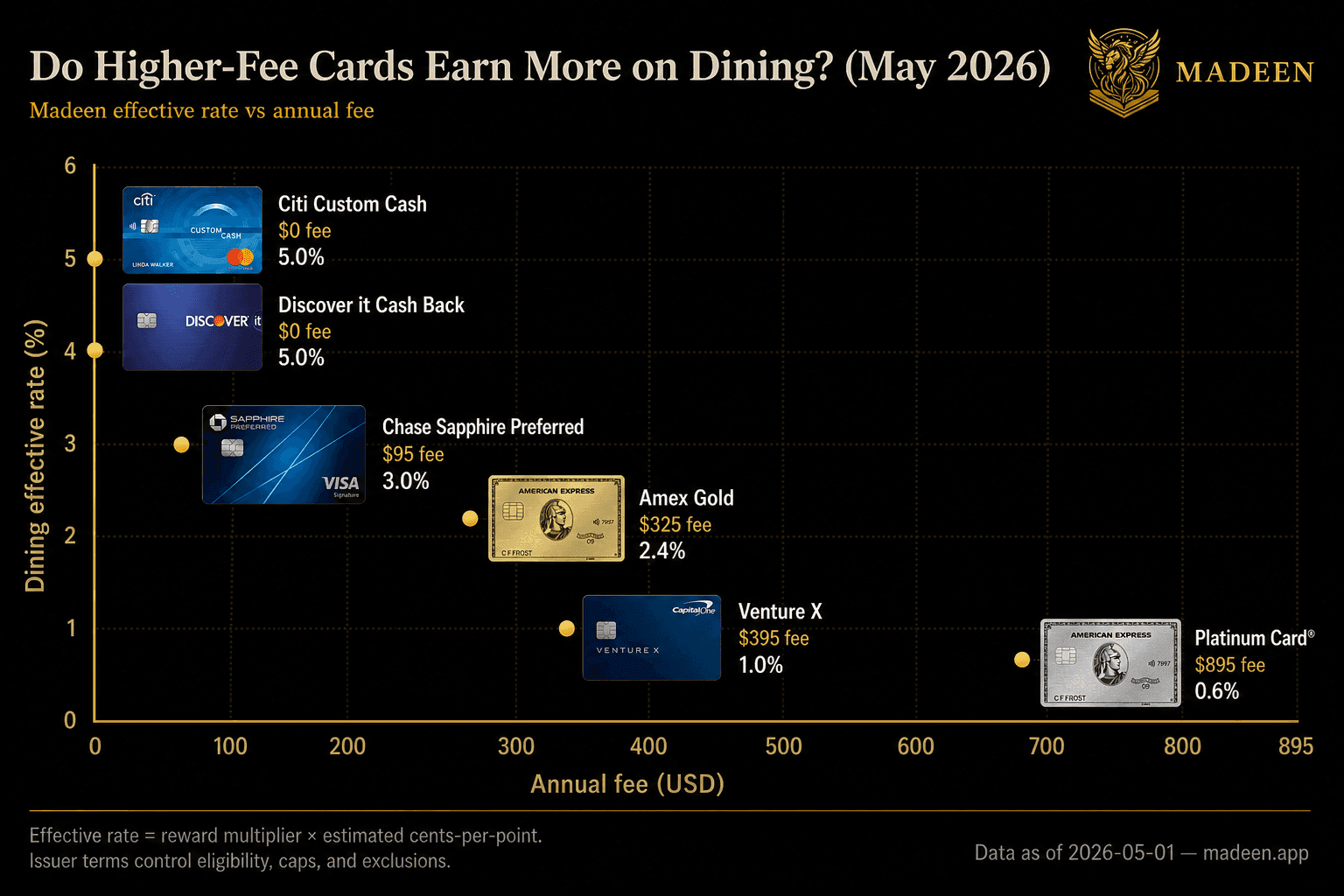

Madeen’s current in-app fallback catalog includes annual-fee data for 3,944 cards. The fee split is wide: 3,085 cards have a $0 Annual fee, 554 have a fee below $100, 60 fall from $100 to $299, and 245 charge $300 or more. That Madeen catalog analysis is documented in the Card Rules Index, while the editorial methodology explains how Madeen separates issuer-authoritative terms from catalog-backed comparisons. The distribution matters because most fee-card decisions are not “fee card or no rewards.” They are “fee card or one of many no-fee alternatives.”

How do you calculate whether an Annual fee card breaks even?

Use the best no-fee card you would otherwise use as the baseline, then compare the fee card against that card.

The simplest formula is:

Annual fee / extra reward rate = break-even annual spendFor example, suppose a card earns 6% Cash Back in an eligible category and charges a $95 Annual fee. If your no-fee alternative earns 3%, the extra reward rate is 3 percentage points:

$95 / 0.03 = about $3,167 in annual qualifying spendThat means the fee card needs about $3,167 in eligible annual spending in that category before the higher rate beats the fee, assuming the card’s cap and store rules do not reduce the reward. Spend below that, and the no-fee 3% card may be better. Spend above that, and the fee card can pull ahead.

What should count toward Annual fee value?

Count only value you would use without changing your behavior in a costly way. Extra rewards are the cleanest value because they come directly from purchases you already make. Statement credits, airport lounge access, free checked bags, hotel nights, and travel protections can matter, but only when they fit your real plans.

The Consumer Financial Protection Bureau treats fees, rewards, and issuer practices as part of the broader cost and availability of credit in its consumer credit card market reporting. That is a useful reminder to evaluate an Annual fee as a cost that must be offset by real, usable value rather than by the highest advertised reward scenario.

Use this conservative order:

- Extra rewards on normal spending: Compare the fee card with your best no-fee alternative.

- Credits you will definitely use: Count a $300 travel credit only if you would spend that money through the required channel anyway.

- Benefits with real avoided cost: A free checked bag matters if you would otherwise pay that fee.

- Soft perks: Lounge access, status, and convenience can be valuable, but they are easy to overcount.

- Welcome bonus: Useful for year one, but not enough by itself to justify renewal.

Premium cards can be excellent when their credits and benefits match your life. They can also be expensive coupon books if you are forcing spend through portals or merchants you would not otherwise use.

When is a no-annual-fee card better?

A no-annual-fee card is better when the fee card’s extra value is uncertain, capped, difficult to redeem, or tied to categories where you do not spend much.

No-fee cards also reduce decision pressure. A card such as the Capital One Savor can be compelling because the break-even point starts at zero: if an eligible purchase earns useful Cash Back, you are not first climbing out of an annual-fee hole. That does not make it the universal best card, but it makes the comparison honest.

In Madeen’s catalog, no-fee cards are the majority. That is a reminder to compare fee cards against a real no-fee fallback, not against earning nothing.

How should you treat credits, points, and miles?

Treat credits at their usable value and points at a conservative estimated value. Do not count the sticker value if you would not redeem it that way.

For a premium travel card, a $395 Annual fee might look much smaller after a travel credit and anniversary miles. But the credit may require booking through a specific travel portal, and miles are not the same as cash unless you redeem them for value you actually want. If you would not use those benefits naturally, discount them.

For points and miles, write down your assumption. If you value a mile at one cent, 2X miles is roughly a 2% estimated return. If you usually redeem below one cent, the same card is worth less. If you consistently transfer points for high-value travel, it may be worth more. See how to redeem credit card points for portal vs transfer paths before you count aspirational redemption value toward a fee.

Should welcome bonuses change the answer?

Welcome bonuses can make a first-year application attractive, but they should not decide the long-term annual-fee question by themselves. A bonus is temporary; the Annual fee repeats.

Use two separate decisions:

- First year: Does the bonus, required spending, fee, and card fit make sense without overspending?

- Renewal year: Do the ongoing rewards, credits, and benefits beat the fee without the bonus?

This separation helps avoid keeping a card for a past bonus that no longer changes your everyday reward value.

How can Madeen help with annual-fee decisions?

Madeen does not ask for your bank login, card numbers, or transaction history. You select the cards you carry, then Madeen compares their category reward rules locally.

That is useful for annual-fee decisions because the renewal question often starts with everyday categories: groceries, dining, gas, travel, and everything else. If a fee card rarely wins those categories in your actual wallet, the card needs strong credits or benefits to justify staying open. If it wins often and its benefits are easy to use, the fee may be doing real work.

For more on the privacy model, read why Madeen does not ask for your bank login. If you want category-specific examples, start with the guides for groceries, dining, gas, and summer travel when a seasonal trip pushes you toward a fee card. For no-fee break-even examples, compare Citi Double Cash vs Wells Fargo Active Cash, Wells Fargo Active Cash vs Capital One SavorOne, and how to evaluate a welcome bonus before a fee card’s first-year math tempts you. Large welcome-bonus minimum spend can spike credit utilization on a single card — factor limits into renewal math.

What should you do before paying or renewing a fee?

Make a short renewal note before the Annual fee posts:

- List the card’s Annual fee.

- Estimate extra rewards versus your best no-fee alternative.

- Add only credits you used or will clearly use.

- Add benefits that replaced real costs.

- Ignore aspirational perks you did not use last year.

- Keep the card only if the conservative total beats the fee.

Issuer terms are authoritative, and card benefits can change. Before applying for or renewing any card, review the issuer’s current pricing, reward caps, exclusions, and benefit terms.

Related encyclopedia topics

Frequently asked questions

Is a credit card annual fee worth it?

A credit card annual fee is worth it only when the extra rewards, credits, and benefits you will actually use are worth more than the fee compared with a no-annual-fee alternative.

How do you calculate if an annual fee is worth it?

Compare the fee card with the best no-fee card you would otherwise use, then divide the annual fee by the extra reward rate. Add only credits and perks you will reliably use.

When is a no-annual-fee card better?

A no-annual-fee card is better when your spending is modest, your purchases do not qualify for the fee card's bonus categories, or you would not use the fee card's credits and benefits.

Should welcome bonuses count toward annual fee value?

A welcome bonus can make the first year attractive, but it should not be the only reason to keep a fee card long term. Use ongoing rewards and benefits for the renewal decision.

Can Madeen help compare fee cards without bank login?

Yes. Madeen compares reward rules for the cards you select locally, so you can see which card wins for a category without sharing bank credentials or card numbers.

Sources and notes

- Madeen analysis Madeen card catalog and annual-fee analysis - Madeen Accessed 2026-05-18.

- Methodology Madeen editorial methodology - Madeen Accessed 2026-05-18.

- Regulator The Consumer Credit Card Market - Consumer Financial Protection Bureau Accessed 2026-05-18.

- Issuer terms Capital One Savor Cash Rewards Credit Card - Capital One Accessed 2026-05-01.

- Issuer terms Blue Cash Preferred Card from American Express - American Express Accessed 2026-05-01.

- Issuer terms Blue Cash Preferred Card terms and disclosures - American Express Accessed 2026-05-01.

- Issuer terms Capital One Venture X Rewards Credit Card - Capital One Accessed 2026-05-01.